Blog

Blog

Post-OBBB, VPPs are Primed to Meet New Energy Challenges

Post-OBBB, VPPs are Primed to Meet New Energy Challenges

Collin Smith, Regulatory Affairs Manager

The last few months have been rough for the clean energy sector. The recently-passed One Big Beautiful Bill (OBBB) Act ended tax credits for wind and solar after 2027, several years ahead of schedule. Other zero-carbon generation technologies like batteries, nuclear, and geothermal fared a bit better but still saw new tax credit restrictions put in place. Analysis by Princeton has found that, by 2035, these policies will reduce U.S. clean energy production in 2035 by 820 TWh and increase average household energy costs by $280 a year.

But while the bill ended incentives for clean generation, it may have unintentionally created the ideal conditions to supercharge the demand response (DR) sector. OBBB’s passage comes alongside a paradigm shift in the U.S. energy landscape, one characterized by massive recent load growth from data centers and accelerated electrification. With clean generation forecasts falling and new gas plants still tied up with production constraints until at least 2030, utilities are searching for any options available to meet this projected demand. Virtual power plants (VPPs) are the fastest, most affordable solution to fill that capacity gap.

VPPs Help Keep DERs Moving Forward

For many of our distributed energy resource (DER) technology partners – especially those focused on hardware deployment – the OBBB’s new tax credit restrictions introduce potential headwinds. But, VPP revenue can provide a counterweight, creating near-term opportunities for DER providers to create new value from their assets.

VPPs are largely resilient to the OBBB’s policy changes because they never received any direct federal tax credits to begin with. Within the policy space, DR is mostly impacted by state regulation and wholesale market rules, so nothing in the OBBB changed the ability for VPPs to expand in the short term. Similarly, since the primary “product” in VPPs is the software that ties an aggregation of flexible devices together, the industry is less impacted by tariffs.

Over the long term, tariffs and tax credit cuts will likely slow deployments of electric vehicles (EVs) and distributed batteries in the U.S., which will reduce the number of these types of flexible devices that can participate in VPPs. But at the moment, there’s plenty of potential to expand VPPs in the U.S. simply by taking advantage of flexible devices that have already been deployed. A 2024 report from Wood MacKenzie showed that the US already has over 100 GW of flexible resources ready to be aggregated into VPPs, but less than 20% of those are currently participating in a DR program.

This means a large latent resource is sitting untapped – one that could provide new revenue streams for DER providers via their existing assets, even if new installations slow. Since these resources are already installed, they can be brought online much faster and at far less cost than either utility-scale batteries or gas plants.

One of the greatest opportunities is in the residential sector, where Wood MacKenzie estimates only 9% of eligible customers are enrolled in DR. As utilities start to look for new solutions to meet their rapid load growth projections, opportunities for DER providers to help meet these demands with customer-sited resources are coming to the fore.

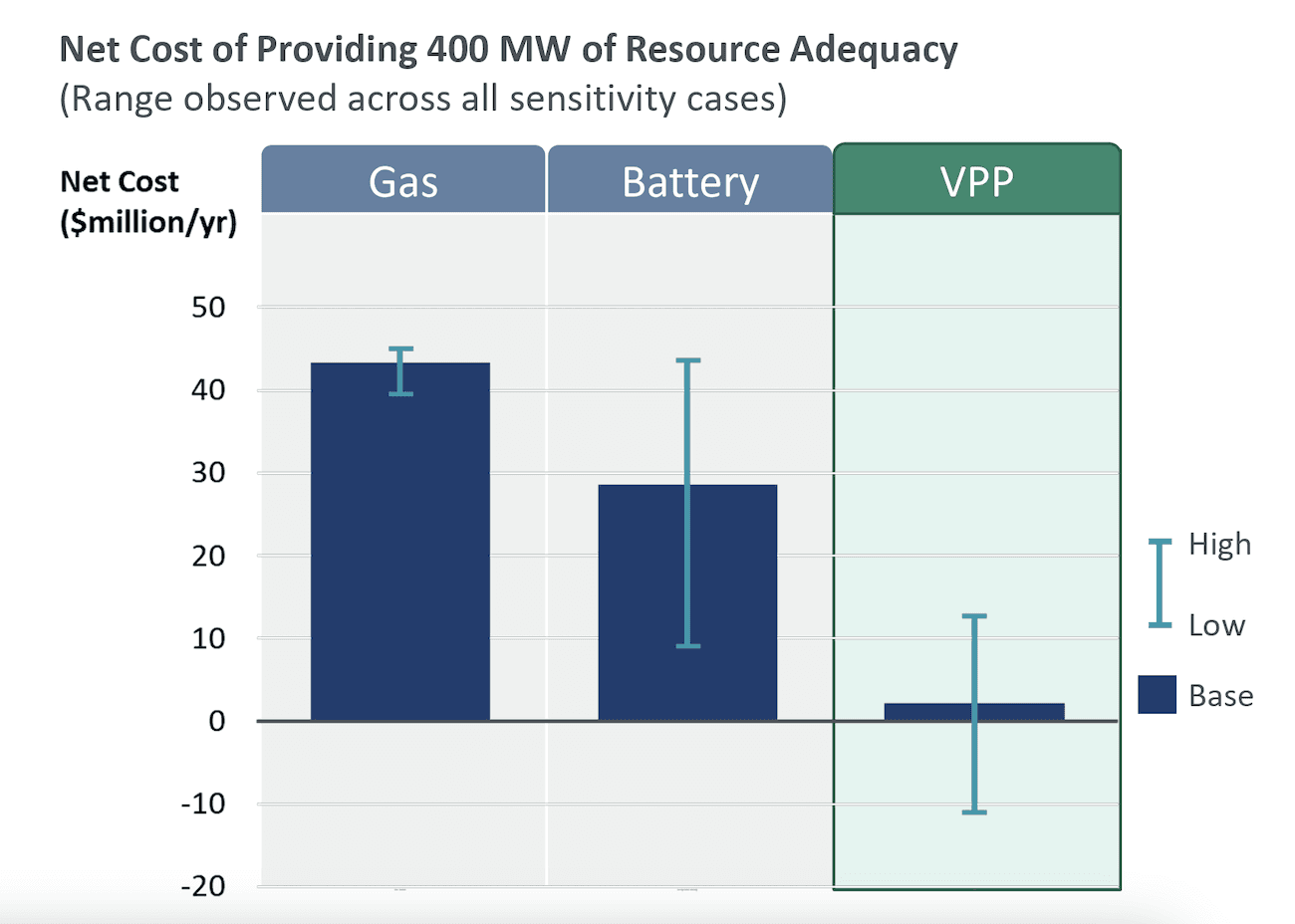

The chart below shows recent analysis by the Brattle Group comparing the cost of procuring capacity from gas plants, utility-scale batteries, and VPPs. Across almost all scenarios, VPPs were less expensive than batteries, and they consistently came in significantly cheaper than gas.

Source: Brattle Group, Real Reliability: The Value of Virtual Power

By expanding VPP participation, DER providers can help customers unlock more value from existing devices — and position themselves as part of the solution to grid reliability and affordability challenges.

It’s All About Peak Load

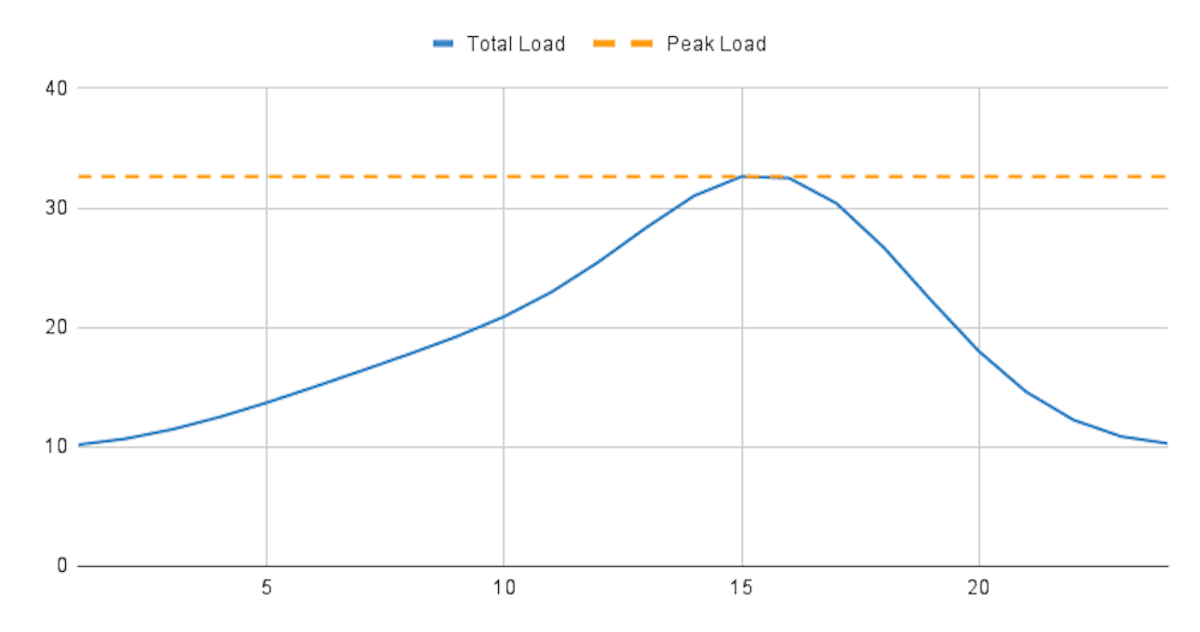

Some might assume that VPPs — which reduce energy use during a limited number of hours of the day — can’t help solve 24/7 challenges like data center growth. This assumption ignores the way that grid operators actually plan resource procurement. Operators are required to procure generation to meet the highest possible demand that they could see on the system, which is usually set by a demand “peak” that occurs in the mid-late afternoon.

The graph below shows a hypothetical daily load curve, with a “peak load” line demonstrating the maximum amount of power demand that utilities need to meet.

Sample Daily Load Curve

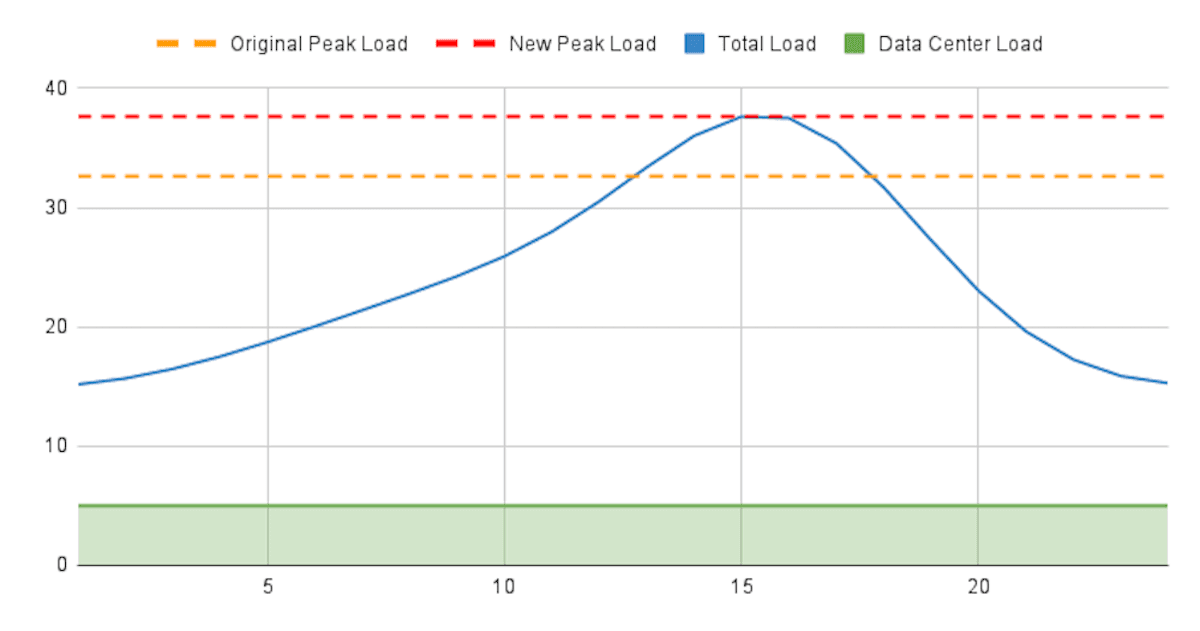

If new data centers raise demand around the clock, then grid operators are required to procure extra MW to meet the new peak.

Sample Load Curve With New Data Center Load

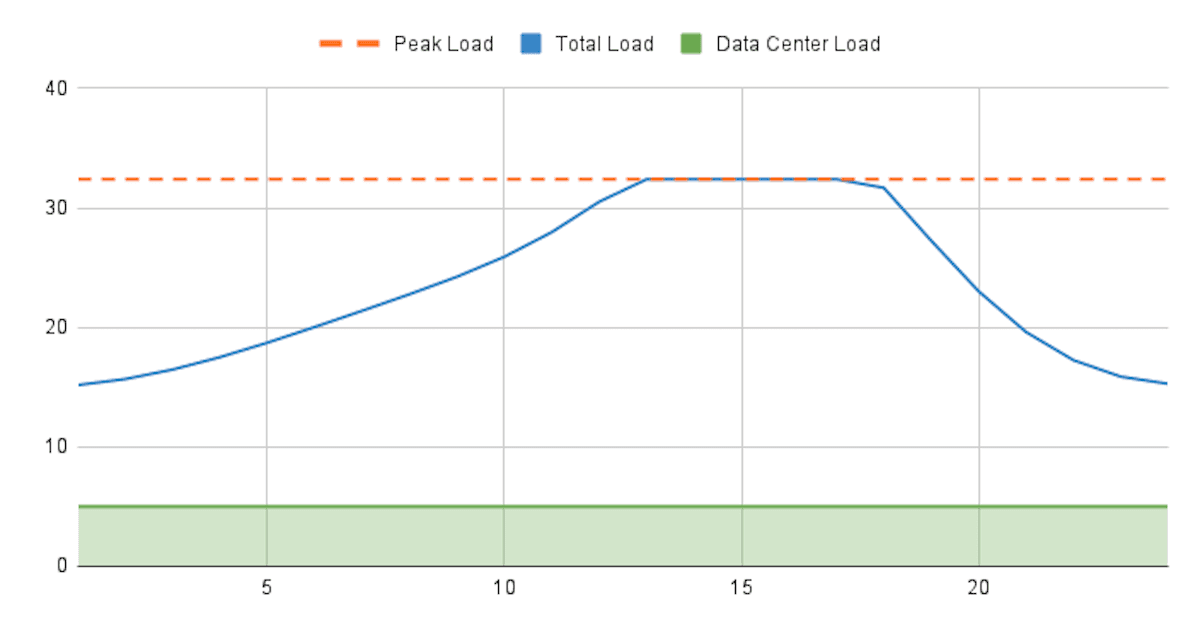

VPPs can help shave those peaks, allowing the grid to accommodate new data center load growth while avoiding a need to build new, expensive fossil fuel infrastructure.

Sample Load Curve With New Data Center Load and Peak Shaving

Ultimately, meeting load growth is always a matter of meeting peak load. A recent study by Duke University showed that the existing U.S. power system could accommodate 100 GW of new load if that load were able to curtail just 0.5% of the year. In other words, addressing overall load growth from these sources is easy if you’re able to manage the system peaks. Fortunately, managing peaks—both on a daily basis or during emergency situations—is exactly what VPPs are designed to do.

Pay No Attention To That Man Behind The Curtain

Based on the headlines, it’s easy to see the OBBB as the main force directing the energy sector in the future. In reality, while federal policy is impactful, the most influential development over the next decade will be the sector’s switch back to a high demand growth scenario. The last time the U.S. saw such immense load projections was in the 70s, when home air conditioning took off. Now, after 50 years of relatively flat electricity demand, grid operators are waking up to the reality that new demand is coming faster than they might be able to meet it.

In this new normal, VPPs can emerge as a star player. With federal policy and production constraints decreasing the speed and increasing the cost with which utilities and power plant developers can put steel in the ground, software-based solutions that can be set up quickly and tap into the vast network of unutilized flexible load capabilities are going to be incredibly attractive. This is an all-hand-on-deck situation, and VPPs just happen to be the load growth solution that’s most readily at hand.

The last few months have been rough for the clean energy sector. The recently-passed One Big Beautiful Bill (OBBB) Act ended tax credits for wind and solar after 2027, several years ahead of schedule. Other zero-carbon generation technologies like batteries, nuclear, and geothermal fared a bit better but still saw new tax credit restrictions put in place. Analysis by Princeton has found that, by 2035, these policies will reduce U.S. clean energy production in 2035 by 820 TWh and increase average household energy costs by $280 a year.

But while the bill ended incentives for clean generation, it may have unintentionally created the ideal conditions to supercharge the demand response (DR) sector. OBBB’s passage comes alongside a paradigm shift in the U.S. energy landscape, one characterized by massive recent load growth from data centers and accelerated electrification. With clean generation forecasts falling and new gas plants still tied up with production constraints until at least 2030, utilities are searching for any options available to meet this projected demand. Virtual power plants (VPPs) are the fastest, most affordable solution to fill that capacity gap.

VPPs Help Keep DERs Moving Forward

For many of our distributed energy resource (DER) technology partners – especially those focused on hardware deployment – the OBBB’s new tax credit restrictions introduce potential headwinds. But, VPP revenue can provide a counterweight, creating near-term opportunities for DER providers to create new value from their assets.

VPPs are largely resilient to the OBBB’s policy changes because they never received any direct federal tax credits to begin with. Within the policy space, DR is mostly impacted by state regulation and wholesale market rules, so nothing in the OBBB changed the ability for VPPs to expand in the short term. Similarly, since the primary “product” in VPPs is the software that ties an aggregation of flexible devices together, the industry is less impacted by tariffs.

Over the long term, tariffs and tax credit cuts will likely slow deployments of electric vehicles (EVs) and distributed batteries in the U.S., which will reduce the number of these types of flexible devices that can participate in VPPs. But at the moment, there’s plenty of potential to expand VPPs in the U.S. simply by taking advantage of flexible devices that have already been deployed. A 2024 report from Wood MacKenzie showed that the US already has over 100 GW of flexible resources ready to be aggregated into VPPs, but less than 20% of those are currently participating in a DR program.

This means a large latent resource is sitting untapped – one that could provide new revenue streams for DER providers via their existing assets, even if new installations slow. Since these resources are already installed, they can be brought online much faster and at far less cost than either utility-scale batteries or gas plants.

One of the greatest opportunities is in the residential sector, where Wood MacKenzie estimates only 9% of eligible customers are enrolled in DR. As utilities start to look for new solutions to meet their rapid load growth projections, opportunities for DER providers to help meet these demands with customer-sited resources are coming to the fore.

The chart below shows recent analysis by the Brattle Group comparing the cost of procuring capacity from gas plants, utility-scale batteries, and VPPs. Across almost all scenarios, VPPs were less expensive than batteries, and they consistently came in significantly cheaper than gas.

Source: Brattle Group, Real Reliability: The Value of Virtual Power

By expanding VPP participation, DER providers can help customers unlock more value from existing devices — and position themselves as part of the solution to grid reliability and affordability challenges.

It’s All About Peak Load

Some might assume that VPPs — which reduce energy use during a limited number of hours of the day — can’t help solve 24/7 challenges like data center growth. This assumption ignores the way that grid operators actually plan resource procurement. Operators are required to procure generation to meet the highest possible demand that they could see on the system, which is usually set by a demand “peak” that occurs in the mid-late afternoon.

The graph below shows a hypothetical daily load curve, with a “peak load” line demonstrating the maximum amount of power demand that utilities need to meet.

Sample Daily Load Curve

If new data centers raise demand around the clock, then grid operators are required to procure extra MW to meet the new peak.

Sample Load Curve With New Data Center Load

VPPs can help shave those peaks, allowing the grid to accommodate new data center load growth while avoiding a need to build new, expensive fossil fuel infrastructure.

Sample Load Curve With New Data Center Load and Peak Shaving

Ultimately, meeting load growth is always a matter of meeting peak load. A recent study by Duke University showed that the existing U.S. power system could accommodate 100 GW of new load if that load were able to curtail just 0.5% of the year. In other words, addressing overall load growth from these sources is easy if you’re able to manage the system peaks. Fortunately, managing peaks—both on a daily basis or during emergency situations—is exactly what VPPs are designed to do.

Pay No Attention To That Man Behind The Curtain

Based on the headlines, it’s easy to see the OBBB as the main force directing the energy sector in the future. In reality, while federal policy is impactful, the most influential development over the next decade will be the sector’s switch back to a high demand growth scenario. The last time the U.S. saw such immense load projections was in the 70s, when home air conditioning took off. Now, after 50 years of relatively flat electricity demand, grid operators are waking up to the reality that new demand is coming faster than they might be able to meet it.

In this new normal, VPPs can emerge as a star player. With federal policy and production constraints decreasing the speed and increasing the cost with which utilities and power plant developers can put steel in the ground, software-based solutions that can be set up quickly and tap into the vast network of unutilized flexible load capabilities are going to be incredibly attractive. This is an all-hand-on-deck situation, and VPPs just happen to be the load growth solution that’s most readily at hand.